Our local market still remains very active with many buyers searching for their ideal home and trying to buy before the holidays. We hope you all have a great Halloween this coming weekend.

Maya Sewald, DRE #00993290 Jason Sewald, DRE #01732384

Welcome to our October newsletter, where we’ll explore residential real estate trends in Silicon Valley and across the nation. This month, we examine the state of the U.S. housing market now that much-needed supply has come to the market. We also explore why the worker shortage may not be as detrimental to the economy as was originally expected because of the renewed growth of entrepreneurship.

With the increase in supply, we’ll probably see the beginning of some market cooling — but in the context of the hottest housing market in history. Housing inventory in the United States continued to rise in August, up 30% from the record low in April 2021. We’re happy to see more homes on the market because they will help satiate the high buyer demand. Although this increase in housing inventory is meaningful, there are still 74% fewer homes on the market than a year ago. The housing market will likely start to see some price corrections as it returns to a steadier state of growth.

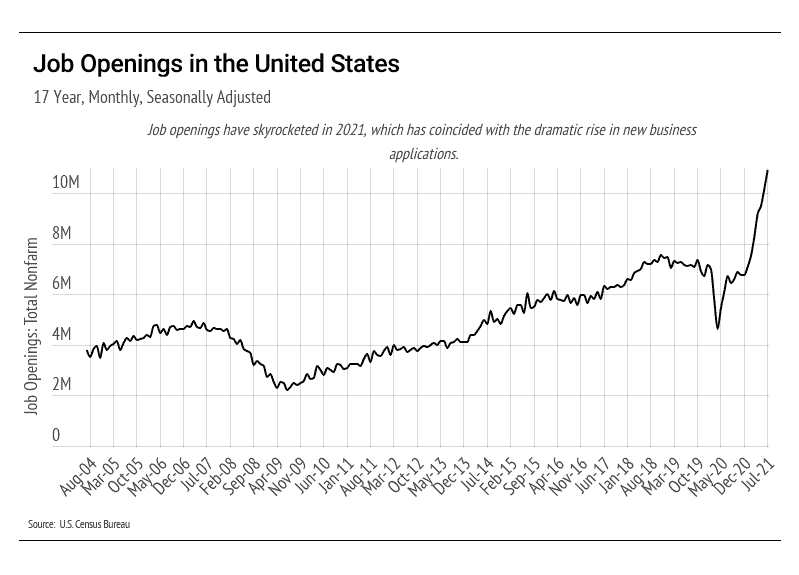

While we, at first, worried that the worker shortage could hurt the economy, it looks like the rise in entrepreneurship is helping to boost production and improve the economy. We often look at jobs to gauge the health of the economy: more employed workers usually means more production and more wealth, which, in turn, means appreciating asset prices. For many months, unemployment stood at around 10 million workers; however, we have started to meaningfully close the unemployment gap, and unemployment has been reduced to 8 million workers. As risks from the delta variant wane, we’ll likely see more unemployed workers reentering the workforce.

Despite the high rate of unemployment and record number of job openings, U.S. production is climbing rapidly. In terms of GDP, which is the broadest measure of goods and services produced, our economic recovery could reach where we would likely be if the pandemic had never happened within the next year. It cannot be overstated how rare it would be to return to pre-recession GDP, but we might just get there. A potential factor in the rise of both production and job openings is the resurgence of entrepreneurship, which is often associated with higher production.

We remain committed to providing you with the most current market information so you feel supported and informed in your buying and selling decisions. In order to better explore how the above national trends in the economy and housing market are affecting Silicon Valley, this month’s newsletter will cover the following:

Key Topics and Trends in October: Current trends in the labor force will have long-term effects on the housing market and overall economy.

October Housing Market Updates for Silicon Valley: San Mateo single-family home prices declined, while condo prices reached an all-time high. Home prices in Santa Clara and Santa Cruz are slightly below peak. Elevated sales for single-family homes and condos over the last five months have kept inventory from climbing to last year’s levels.

Key Topics and Trends in October

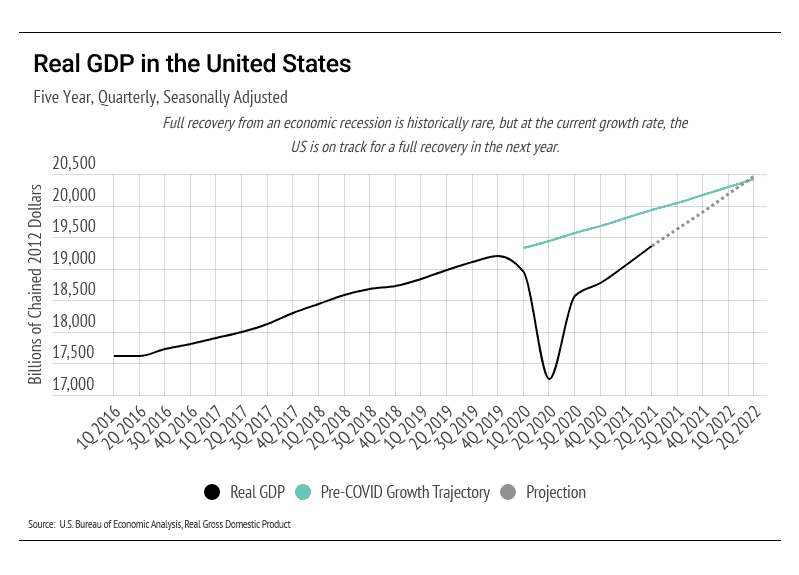

In the long term, employment and GDP reveal much about the economic climate and typically trend with housing prices. GDP, according to the U.S. Bureau of Economic Analysis, gained 1.6% quarter-over-quarter in 2nd Quarter (2Q) 2021, which is about 1% higher than the long-term quarterly growth rate of 0.6%. To get back to pre-pandemic GDP levels, we need to continue to outpace the long-term growth rate. The substantial infusion of cash into the economy has boosted GDP, and we are on pace to fully recover.

The chart below illustrates the cost of the COVID recession and the projection at GDP’s current growth rate. While it depicts U.S. GDP from 2016 to 2Q 2021, it also illustrates economic patterns that occur in all recessions. GDP tends to grow at a fairly consistent rate during economic expansions. The green line exemplifies the expected GDP, had the pandemic never happened. As that green line shows, we are below where GDP was expected to be in 2Q 2021. In other words, we’re still underwater. However, unlike typical recoveries, which return to a steady state of growth but at a lower level, the current growth rate is far higher than normal and should bring us back to our pre-pandemic trajectory by the end of the 2nd Quarter 2022.

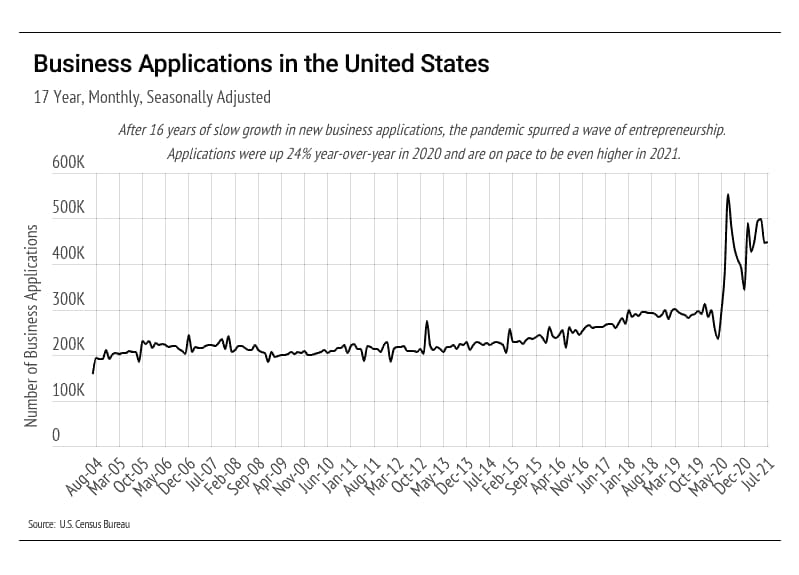

Another large government-sponsored infusion of cash into the economy is very unlikely to happen. We may, however, have another source of economic stimulus: the massive growth in entrepreneurship over the last 16 months. From 2004 to 2019, the United States averaged 2.8 million new business applications per year. In 2020, there were 4.36 million, and in 2021, there have been 3.68 million as of August. This means that over the past 20 months, the United States has seen 8 million new business applications.

The competitive nature of our economy incentivizes new business owners to produce, creating jobs and stimulating growth. While new businesses are not as stable as more mature companies, they are often more nimble than larger companies and can produce with fewer hurdles.

The large number of new business applications may also explain why established companies have found it difficult to fill job openings. It seems that a large number of workers may now be working for themselves. Although the difficulty with hiring employees poses troubling challenges to employers, it thankfully may not indicate a struggling economy.

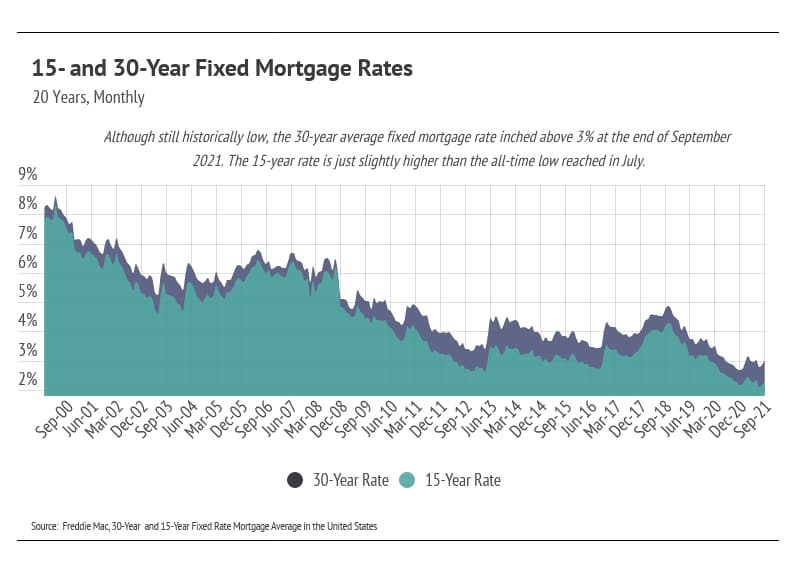

Home prices tend not to experience meteoric rises if the economy is in dire straits. Because home prices have increased so rapidly over the last two years, we can assume that the economy is doing well. In the last five years, housing inventory has decreased by around 940,000 (59%). Over 700,000 of those homes were sold in the last two years alone. Due to the pandemic, housing demand rose to historically high levels and mortgage rates fell to historic lows. As shown in the chart below, we’re currently hovering near all-time low mortgage rates, which will likely remain for the rest of the year. Low rates incentivize buying due to the lower monthly payment.

Even with rising inventory, the market remains competitive for buyers, but conditions are making it an exceptional time for homeowners to sell. Low inventory means sellers will receive multiple offers with fewer concessions. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agents to ensure the transition goes smoothly.

October Housing Market Updates for Silicon Valley

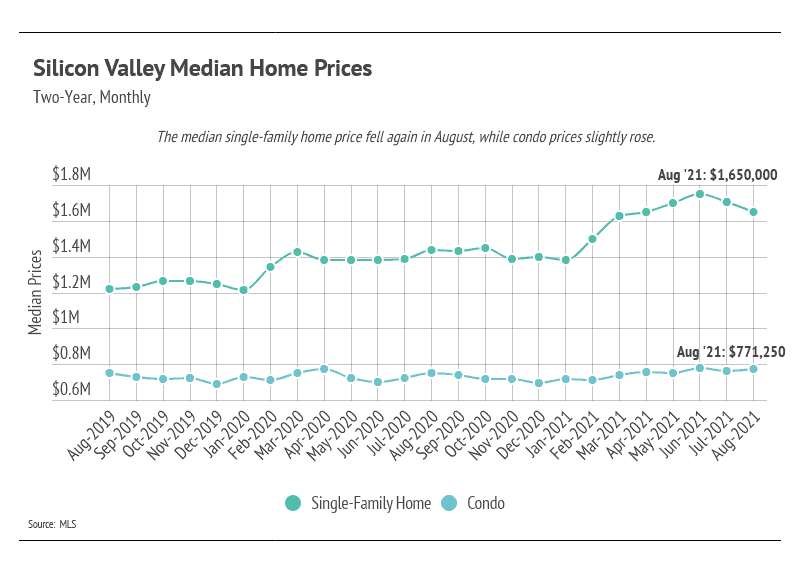

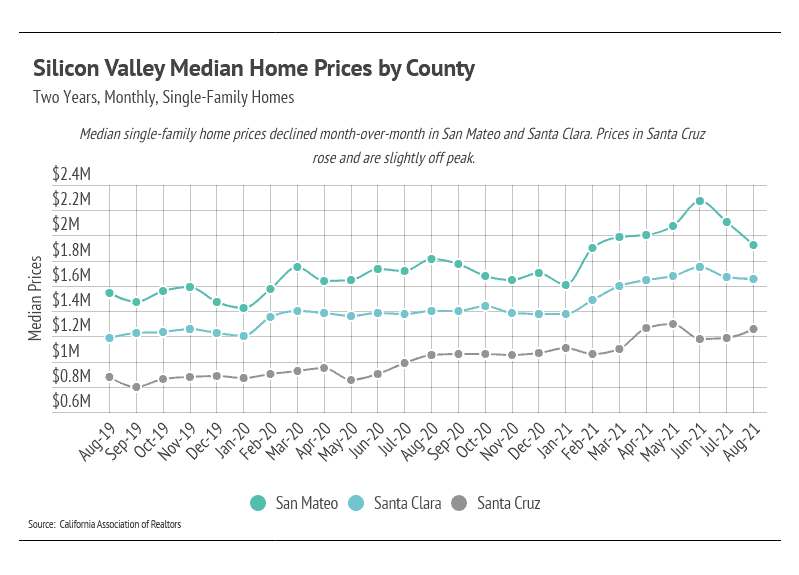

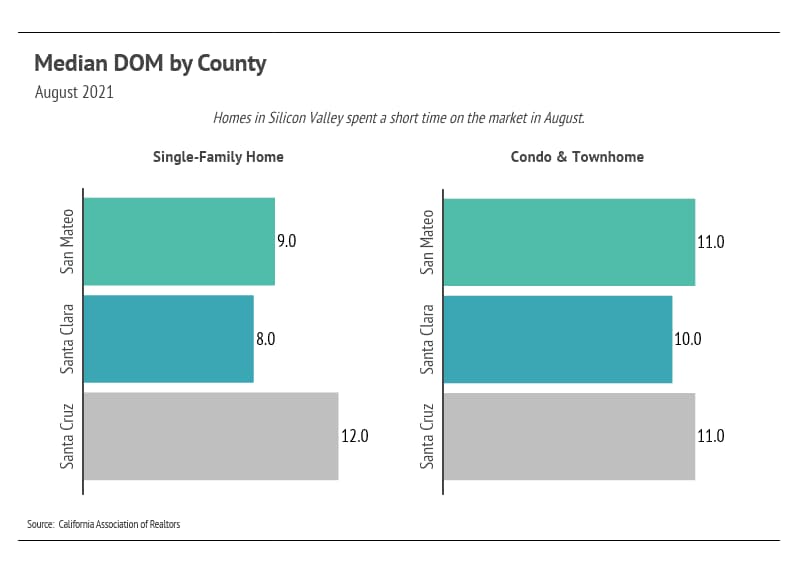

During August 2021, in Silicon Valley, the median single-family home price declined — mostly due to San Mateo County, although Santa Clara prices declined slightly as well. Santa Cruz home prices rose month-over-month, almost returning to an all-time high.

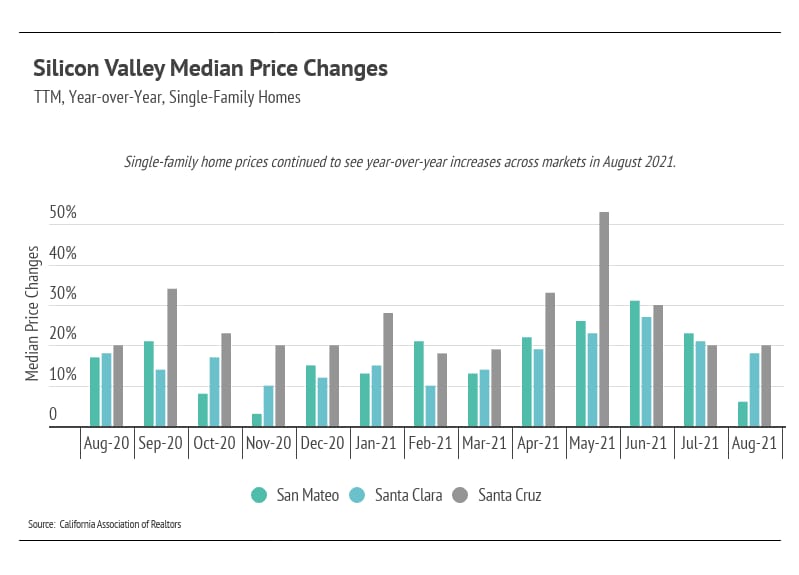

Silicon Valley homes have appreciated year-over-year for the last 12 months.

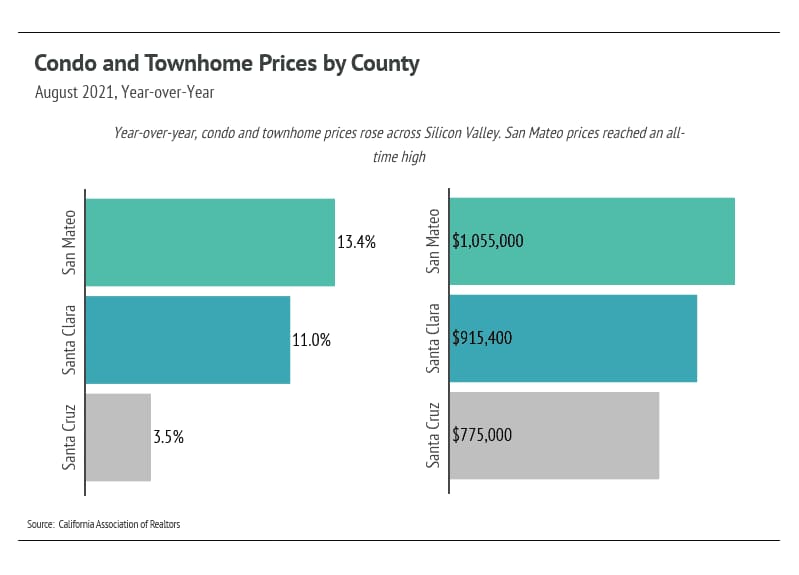

As you can see in the graph below, median condo prices increased in Silicon Valley. San Mateo condos and townhomes reached an all-time high, while Santa Clara and Santa Cruz are slightly below peak.

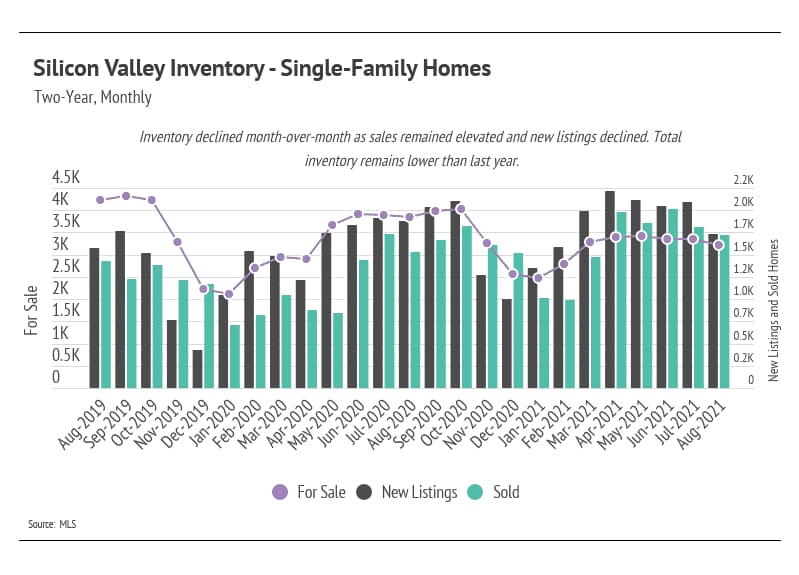

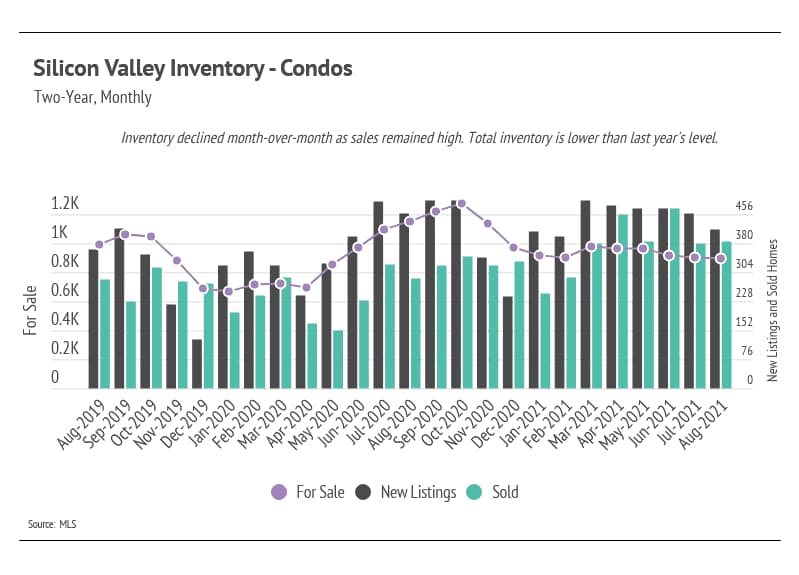

Single-family home inventory began to climb at the start of 2021 in anticipation of the spring season, when more sellers typically come to market, but has begun to decline once again. To gain a full picture of the current market, we must view it in the context of last year. In 2020, fewer people wanted to leave Silicon Valley, while more people wanted to move to the area. This trend drove inventory down to record low levels. New listings, therefore, improve the current market conditions. However, new listings aren’t keeping up with demand. In August 2021, Silicon Valley had 16% fewer homes for sale than it did in August 2020. Furthermore, when we compare the current inventory to August 2019 (pre-pandemic) levels, the number of homes for sale has declined by 24%. The sustained low inventory will likely cause prices to remain stable or appreciate throughout 2021.

The number of condos on the market declined slightly in August 2021 but seems to have stabilized overall. Condo demand remains incredibly high in Silicon Valley, and new listings are selling quickly.

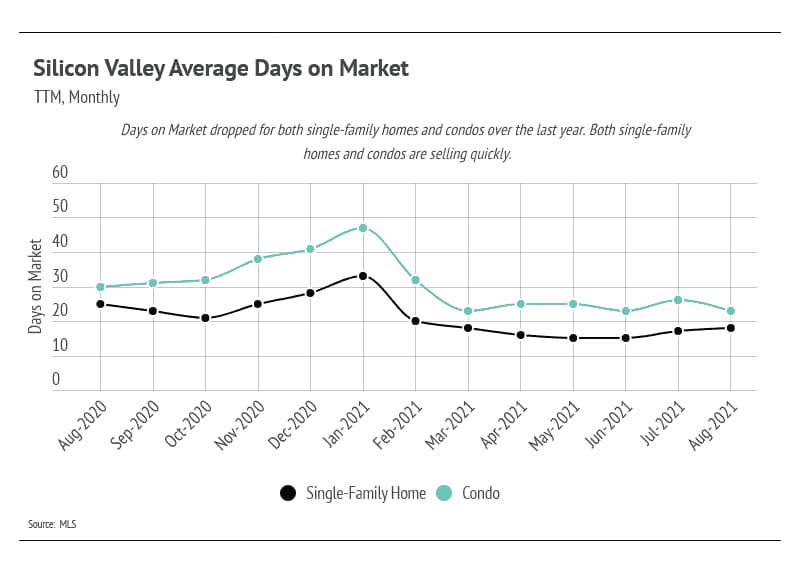

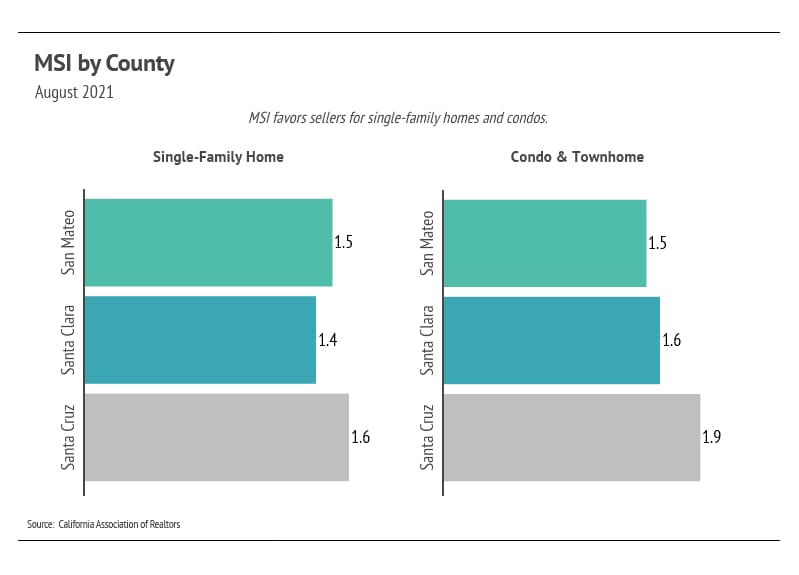

Both single-family homes and condos spent less time on the market in August 2021 than they did in August of last year. As we’ll see, the pace of sales has contributed to the low Months of Supply Inventory (MSI) over the past several months.

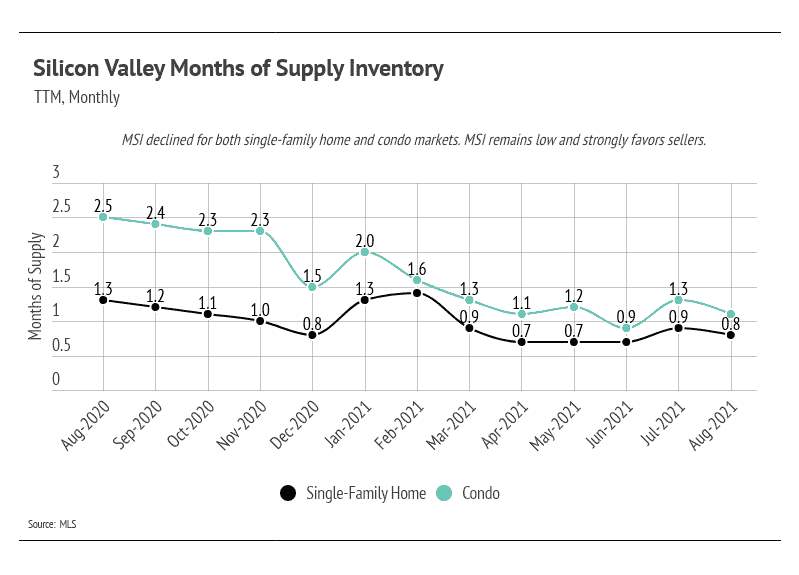

We can use MSI as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). In August 2021, the MSI was unchanged month-over-month, indicating that the market strongly favors sellers.

In summary, the high demand and low supply in Silicon Valley have driven home prices up over the last year, but the huge price appreciation is slowing. Inventory will likely remain historically low this year with the sustained high demand in the area. Overall, the housing market has shown its value through the pandemic and remains one of the most valuable asset classes. The data show that housing has remained consistently strong throughout this period.

We expect the number of new listings to slow in the coming months. However, the current market conditions can withstand a high number of new listings, and more sellers may choose to enter the market to capitalize on the high buyer demand. We expect the high demand to continue, and new houses on the market to sell quickly.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.